The State of Green Hydrogen: Big Promises, Slow Progress

by Pete Rocha, LEC Partners Low Carbon Hydrogen Lead

In 2023 green hydrogen appeared poised to play a major role in the U.S. energy transition. The announcement of the Department of Energy’s (DOE) hydrogen hubs and the Investment Reduction Act’s (IRA) production credit heralded strong policy support. Nearly three years later deployment is slow and green hydrogen remains expensive. While it’s easy to point to changes in Federal policy, the hydrogen sector is also being held back by basic economics, above all: price. Resetting expectations for how hydrogen will evolve in the U.S. would be beneficial.

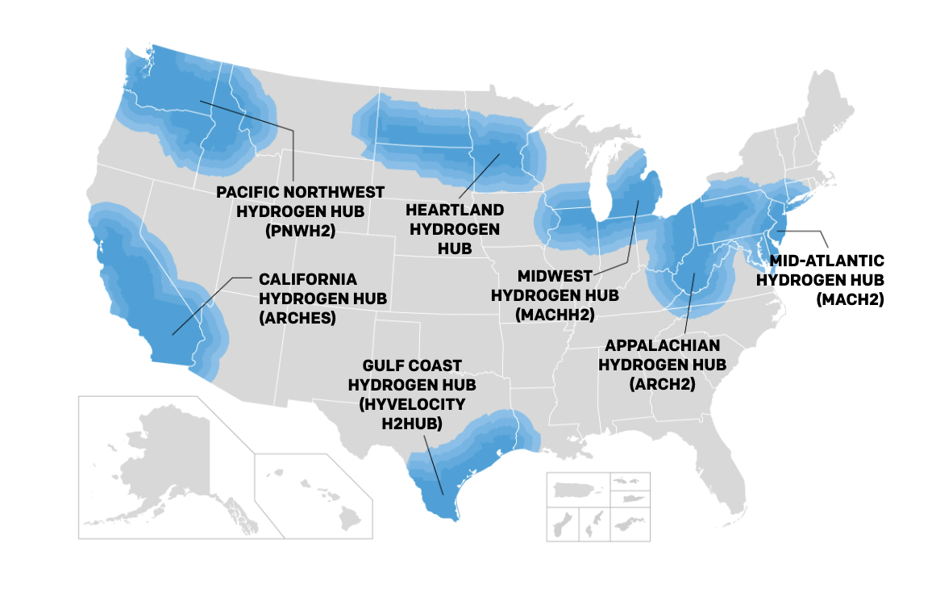

U.S. Hydrogen Hubs as Conceived in 2023 Source: https://www.earthjustice.org

Source: https://www.earthjustice.org

One of the strongest reasons for green hydrogen optimism early in the decade was the DOE’s hydrogen hubs program. The hub concept was designed to build a complete ecosystem for hydrogen development. Rather than just focus on production, the hubs were designed to create a holistic approach to connect hydrogen generation with regional demand and infrastructure required to deliver H2 to market.[1] This idea was backed by USD $8B to develop the hubs, authorized by Congress under the Infrastructure Investment and Jobs Act (IIJA) .[2], and further buttressed by a $USD 3/KG H2 production credit under Section 45V of the Inflation Reduction Act (IRA).[3] In tandem, these policies were designed to both stimulate green hydrogen production (and other forms of hydrogen) and provide meaningful market outlets, which would attract further private investment. This mechanism would create a virtuous cycle where increased demand led to increased scale, lowering prices and thereby creating more demand.

However, like most plans, execution did not strictly follow design. The change of Presidential Administrations is a good place to begin understanding the divergence from the anticipated path forward. The original push for the hydrogen hubs came during the Biden Administration. The Trump Administration had different priorities. Less than a year after the 2024 Presidential election the Department of Energy (DOE) pulled $2.2B in funding designated for the green hydrogen hubs in California and Washington.[4] The other five hubs were paused and ultimately the DOE announced that the remaining hubs would be retained but could be subject to modification.[5] This includes the Mid-Atlantic and Heartland hubs, which included green hydrogen pathways as part of the mix. All the hubs relied on a public-private partnership model to fully build out the infrastructure required for a hydrogen economy. Therefore, the government not only removed funding from the two green hydrogen hubs, it introduced political risk and uncertainty for the remaining hubs where green hydrogen plays a role. Such conditions are not ideal for investment. Finally, the modification of the IRA 45V Hydrogen production credit also likely impacted the trajectory of green hydrogen growth. The One Big Beautiful Bill Act (OBBBA) passed in 2025 accelerated the sunset of the Credit by five years, from 2032 to 2027.[6] All hydrogen production facilities must now break ground by December 31st, 2027, or they will be ineligible for the tax credit. Given the complexity of these large-scale projects from a planning, permitting and financing perspective, and policy uncertainty around green hydrogen, there is a lot of additional risk added by the five-year timeline compression. Policy changes in both the hydrogen hubs funding and the IRA production credit played a major role in the slowing of green hydrogen development in the U.S.

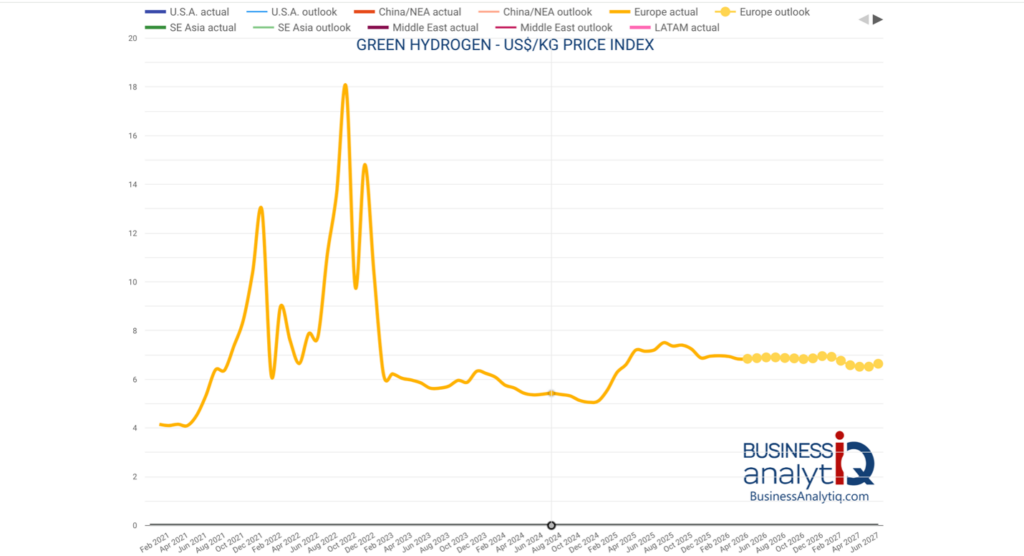

Policy is only part of the story, however; green hydrogen’s sluggish progress also reflects fundamental economics, especially continued high prices. In 2021, the DOE announced a “hydrogen shot” goal to reduce the price of green hydrogen to $1/kg within a decade.[7] However, the price of green hydrogen today in Europe, where there is a functioning market, is between $6-7/kg.[8] As shown in Figure 1 below, this pricing is largely unchanged over the past three years.

Price of green hydrogen in Europe

Source: https://www.businessanalytiq.com

While the price reflects a higher European cost of electricity than found in the U.S., it also demonstrates that industry scale-up has not led to material savings in cost of production. As a result, investment in green hydrogen projects in Europe have also been delayed despite a much friendlier regulatory environment.[9] An argument can be made that the DOE’s hydrogen shot was always a stretch goal and should not have been taken as a reference point for the actual price of hydrogen by 2030. However, the practical effect of failing to make progress on a stated objective is frequently disillusionment, which does nothing to help investor appetite required to move projects forward. Scale and learning will undoubtedly eventually push prices lower; however, a more realistic timeframe of 15-20 years to achieve near price-parity with fossil hydrogen would have better calibrated expectations.

The bigger question now is whether green hydrogen’s promise has faded beyond recovery? Long-term trends still point to relevance for green hydrogen. First, industrial decarbonization remains a priority for governments and corporations. A 2026 PWC report states that a full 82% of companies surveyed have maintained or accelerated their sustainability goals.[10] In industries like steel production, ammonia production, and fuels and chemicals refining green hydrogen still holds the most promise for industrial decarbonization. Green hydrogen still has a potential role in using excess renewables and balancing the grid. Hydrogen can be made from excess (curtailed) renewables, maximizing asset utilization. The hydrogen can be stored for months allowing for grid balancing across weeks and seasons where renewable production can be limited by weather patterns, e.g winters in the U.S. Northeast.[11] Finally, the logic about price reduction with scaling was not wrong, but rather too optimistic. Taken together, these factors suggest that green hydrogen’s long-term promise remains intact, even if the timeline for cost competitiveness and large-scale deployment will likely be longer and more difficult than early advocates expected.

So, the state of green hydrogen in 2026 is much diminished compared to the expectations set several years prior. With the status of the two green hydrogen hubs in limbo and the remaining two subject to modification, the original vision for rapid expansion of the green hydrogen economy in the U.S. has not been achieved. Modifications to the IRA 45V production credit and persistently higher green hydrogen prices have also played a major role in the lack of industry progress. Still, the long-term case for hydrogen remains intact as the sector adjusts to today’s policy and market headwinds. In the meantime, companies and investors will need experienced guidance to navigate an uncertain landscape and position themselves for the eventual scale-up.

[1] https://www.resources.org/common-resources/hydrogen-hubs-helping-ensure-their-success/

[2] https://www.congress.gov/crs-product/R47289

[3] https://www.congress.gov/crs-product/IF12602

[4] https://www.canarymedia.com/articles/hydrogen/hydrogen-hub-cuts-trump-doe-list

[5] https://www.bloomberg.com/news/articles/2026-04-15/us-to-preserve-billions-in-hydrogen-funds-pegged-for-termination

[6] https://kbhenergycenter.utexas.edu/media/blue-hydrogen-and-the-45v-tax-credit-how-to-maintain-american-energy-excellence/

[7] https://grist.org/energy/the-department-of-energy-is-trying-to-make-clean-hydrogen-this-generations-moonshot-earthshot/

[8] https://businessanalytiq.com/procurementanalytics/index/green-hydrogen-price-index/

[9] https://www.ey.com/content/dam/ey-unified-site/ey-com/fr-fr/insights/climate-change-sustainability-services/documents/ey-hyvolution-ey-european-hydrogen-20250214.pdf

[10] https://www.pwc.com/us/en/services/esg/library/decarbonization-strategic-plan.html

[11] https://www.sciencedirect.com/science/article/abs/pii/S0360319924013223

Have some questions?

Not sure where to start?

Let's start a conversation. We're here to help you navigate

the bioeconomy with confidence.