What Can Ethanol Plant Owners do to Thrive in the Ethanol Business Today?

By Mike Sticklen & Dr. Doug Rivers LEC Partners

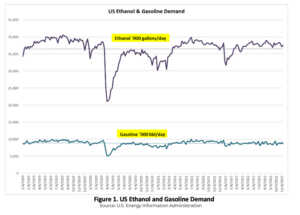

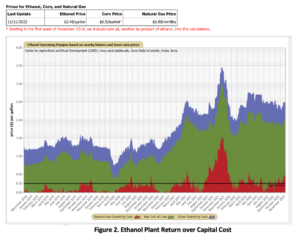

The US ethanol industry is faced with flat volume (Fig. 1) and mediocre returns on capital (Fig. 2). There are several strategic opportunities available to return to revenue growth and improve returns to shareholders. The strategies can be grouped into three categories.

-

- Fuel Ethanol carbon intensity reduction,

- Product and market diversification

- Feedstock diversification

- Fuel Ethanol Carbon Intensity Reduction

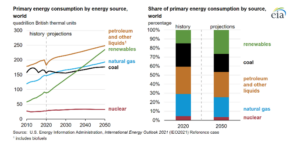

Despite the push for transportation electrification, the US Energy Information Agency (IEA) forecasts that market demand for liquid fuels will grow globally, especially demand for lower carbon intensity (CI) liquid fuels such as ethanol, renewable diesel, renewable gasoline, and sustainable aviation fuel (see Fig. 3). Liquid fuel growth will predominate in Asia with the Americas and Europe remaining flat. This will create an opportunity for low-cost, low-carbon intensity ethanol producers in the US to continue increasing exports and grow domestically with higher ethanol blends such as E-15. Both favorable CI and high-octane rating values should result in demand growth for bio-based fuels.

Figure 3. Global Liquid Fuels Demand Projections

The recent confirmation by US EPA regarding RVO blending obligations under the Renewable Fuel Standard (RFS) for the next 3 years, US corn ethanol production will be basically flat at 15.25 billion gallons per year. The US ethanol industry is capable of producing more than 17 billion gallons per year. The RFS has outlived its benefit to US society and should be abandoned and replaced by low-carbon fuel standards in multiple states. The recently passed Inflation Reduction Act has added production tax credit incentives of 2 cents per gallon for each CI point below 50 gCO2/MJ.

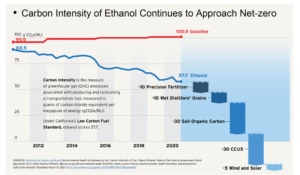

US and Brazil ethanol producers are well positioned to capitalize on the global growth provided their ethanol carbon intensity is reduced from the mid-50 gCO2/MJ to low 10’s gCO2/MJ (see Fig. 4). More than 50% of the US ethanol industry has committed to achieving this via CO2 geological sequestration which generates value through 45Q tax credits and LCFS carbon credits. Ethanol plants that are located near proposed CO2 pipelines are well positioned. The new CO2 pipelines are facing some pushback from some stakeholders due to perceived safety and land eminent domain concerns, however, the pipelines will get built. There are both huge climate-change benefits and economic benefits to be gained. Ethanol plants that are located too far from the announced pipelines or local suitable geology will need to look to alternative carbon reduction solutions including energy efficiency improvements, renewable gas and renewable power generation, and regenerative agriculture with their local corn suppliers.

Figure 4. Corn Ethanol Plant Carbon Intensity Reduction Potential

2. Co-Product Diversification

a. Protein Feed Ingredients and Corn Oil

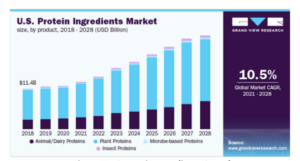

Market demand for protein will continue to grow at over 10% per year over the next decade (see Fig. 5). Ethanol plants are a potential protein factory combining the value of corn protein and yeast protein. The animal feed industry is ready for enhanced corn fermentation protein separation technologies and animal protein feed markets for pet food, aquaculture, poultry, and swine are learning to optimize their feed rations with these ingredients. Technologies such as Fluid Quip’s MSC™, ICM’s AST™, Harvesting Technology’s CoProMax™, and Marquis ProCap™ are being commercialized rapidly. Each of these process additions results in 20-50% corn oil yield improvements. The outlook for higher renewable corn oil demand continuing to grow in support of Renewable Diesel demand will make for continued strong DCO prices and improved profitability. Renewable diesel production will surpass biodiesel production in 2023.

Feed protein quality targets need to be greater than 50% as-sold content with yields of 3 to 4 pounds per bushel of corn. The amino acid profile is important along with excellent quality and consistency. This will require a step-change for many ethanol plants in process control, process monitoring, Food-Safety Modernize Act(FMSA) compliance and good-manufacturing practices (GMP). This will enable the new corn fermentation protein products to be sold at values equivalent to soybean meal and in some applications approaching corn gluten meal. With the large increase in demand and value for soybean oil for renewable diesel feedstock, it remains to be seen how that will affect soybean meal coproduction and market value.

Figure 5. US Protein Ingredients Growth

b. Ethanol to Sustainable Aviation Fuel.

The aviation fuel grand challenge alongside the demand from airline companies for sustainable aviation fuel (SAF) is creating a growth opportunity for ethanol. SAF can be produced via several alternative technologies including hydro-processing of fats, oils and greases, biomass gasification/Fischer-Tropsch conversion and alcohol to SAF. Alcohol to SAF can be from ethanol or higher alcohols like iso-butanol.

Higher alcohols including Gevo’s process have favorable conversion yields compared to ethanol. However, ethanol production cost, which accounts for about 80% of SAF total cost, levels the playing field. The larger ethanol plants have sufficient capacity to provide capital economies of scale for the downstream conversion processes (see Fig. 6). Ethanol from corn starch or sugar will continue to provide superior SAF economics due to low feedstock costs and low carbon intensity provided ethanol plants continue forward with CI reduction commitments. Airlines are interested in cellulosic ethanol pathways due to perceived sustainability advantages, however, the reality is that ethanol from starch and sugars will provide competitive carbon reduction benefits with lower production costs. Existing corn and sugar ethanol plants have a 10-20% incremental capacity potential through debottlenecking and the corn starch supply will continue to grow as a result of crop seed technology advances. Starch production per acre of land will grow along with continually improving crop yields and inputs that will reduce the carbon intensity of row crops and ensure supply for both food and fuel.

Figure 6. Ethanol to SAF process

c. Renewable Methanol

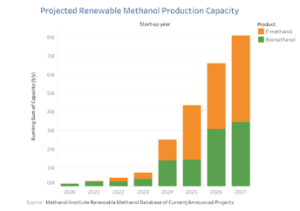

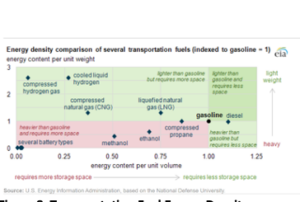

The newly created production tax credit for renewable or green hydrogen has incentivized an opportunity to combine hydrogen with ethanol plant CO2 to produce renewable methanol. Global renewable methanol is forecasted to grow to over 8 million tons per year or 2.7 billion gallons per year by 2027. (see Fig. 7) With low-cost renewable hydrogen and clean biogenic CO2 from ethanol plants, this chemical or fuel is an alternative means to reduce ethanol carbon intensity while producing a valuable co-product. The economics depend on continuously improving renewable hydrogen production costs and the traditional natural gas-based methanol production alternative. The energy density of methanol as a transportation fuel is inferior to ethanol. (see Fig. 8) therefore renewable methanol use will be targeted at non-transportation sectors.

Figure 7. Renewable Methanol Forecast

Figure 8. Transportation Fuel Energy Density

d) Renewable Natural Gas

Renewable natural gas (RNG) from ethanol plant syrup and corn fiber is starting to gain traction with companies like Verbio producing RNG at their Nevada, Iowa facility. Verbio’s RNG is produced via anaerobic digestion of biomass including corn stover and syrup. It is cleaned up and pumped into nearby natural gas pipelines. The RNG qualifies for low-carbon fuel in California along with Advanced RFS credits.

e. Bio-based Plastics

Packaging producers and consumer products companies with extended producer responsibility (EPR) are beginning to drive growth in bio-based plastics with moderate growth of about 5% per year. This is an emerging alternative to producing ethanol from sugar or starch. It remains to be seen whether consumers will be willing to pay a premium price for renewable plastics to justify investments. Bio-based traditional plastics including polyethylene from ethanol and bio-ethylene and PLA and PHA from clean sugars are seeing some new growth. Clean sugar production on the front end of dry-mill ethanol plants is being developed by Fluidquip Technologies at Green Plains Renewable Energy’s Shenandoah, Iowa ethanol plant. The sugar solutions will be cost-competitive with corn-wet-mill dextrose.

f. Feedstock Diversification

Biomass feedstocks for ethanol continue to have interest from potential investors. While technology developers continue to strive for viable Generation 2 cellulosic ethanol processes with milder pre-treatment processes and improved cellulase enzymes, the underlying production economics compared to corn starch and sugar-based ethanol will continue to be unfavorable. Unit capital and conversion cost per gallon for cellulosic ethanol will continue to be 2-3 times higher and delivered biomass cost will be around 70% of the price of corn; however, inferior yields will pretty much offset any price advantage. Cellulosic plant scale will also be disadvantaged. Cellulosic ethanol pathways have CI scores in the low 20’s gCO2/MJ and with fermentation, CO2 capture can be negative. Corn and sugar ethanol with CCUS(carbon capture, utilization, and storage), renewable power and crop input improvements can approach low 10’s gCO2/MJ. The incremental CI benefit of cellulosic feedstock will not offset the capital and production cost disadvantage. Keep an eye on evolving technology from players like Clariant and Saffire Renewables/D3MAX, however, do not be in a hurry to invest in cellulosic feedstocks.

About the Authors:

Mike Sticklen has many years of experience in renewables and polymers, including a variety of leadership roles with Flint Hills Resources, Hawkeye Renewables, Dow Chemical, and DuPont. His most recent experience includes 15 years in fuel ethanol, protein co-products and biodiesel operations, engineering & technology. He is a Project Director at LEC Partners, overseeing matters involving ethanol, protein feed ingredients, plastics, and due diligence.

Dr. Doug Rivers has 45 years of recognized success developing, scaling, optimizing, and commercializing bioprocess technologies. Before joining LEC, Dr. Rivers was the corporate director of R&D at ICM. He was responsible for developing new and improved bioprocess technology to produce ethanol, other liquid fuels such as isobutanol, renewable chemicals, and animal feed co-products from corn, milo, and cellulosic feedstocks. He is a Project Director at LEC Partners, overseeing matters involving bioprocess development, fermentation, ethanol, enzymes, cellulose conversion, and renewable chemicals.

Have some questions?

Not sure where to start?

Let's start a conversation. We're here to help you navigate

the bioeconomy with confidence.